How to Maintain Non-Profit Status for a Charitable Foundation

Cost of services:

Reviews of our Clients

A charitable foundation can operate for years, attract resources, and report on completed projects, only to suddenly receive a decision excluding it from the Register of Non-Profit Institutions and Organizations. No major scandals. No “schemes.” Just a formal violation that the management did not consider critical.

Non-profit status is often perceived as a guaranteed attribute of charitable activity. In reality, it is a tax regime that exists only as long as the foundation complies with the legal requirements every day. Even a single systemic mistake can result in the organization being transferred to the general taxation system, with additional tax liabilities assessed.

We support charitable foundations during inspections and see a clear pattern: the vast majority of status losses are not caused by abuse, but by managerial inattention to detail. A charter that was not updated on time, incorrectly documented payments, or an expansion of aid areas without proper legal formalization, and the tax authority may qualify this as a violation of the non-profit criteria.

In this article, we will explain why charitable foundations lose their non-profit status, which provisions of the Tax Code of Ukraine, hereinafter referred to as the TCU, become critical during inspections, and how to organize operations so that the status remains protected, along with the foundation’s reputation and donor funds.

You might also like: Can Volunteers Receive a Deferment from Conscription?

Non-Profit Status of a Charitable Foundation: Tax “Immunity” or an Area of Constant Control?

Foundation managers often equate state registration with automatic tax “immunity.” But these are two different legal areas, so it is necessary to clearly distinguish between the state registration of a charitable organization and its non-profit status. The first gives the right to be called a foundation. The second, and most importantly, allows the organization not to pay corporate income tax.

So, non-profit status is a separate tax decision. While an organization is registered only once, compliance with non-profit criteria must be confirmed continuously through the structure of the charter, the financial model, and actual operations.

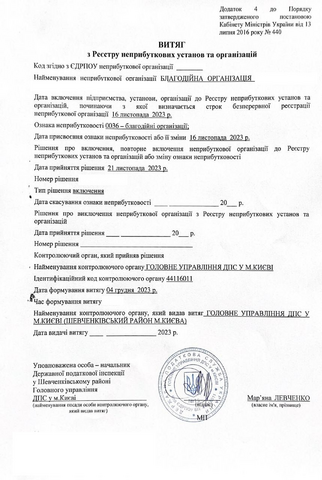

Non-profit status is granted by the State Tax Service of Ukraine only if the organization fully meets the requirements of Article 133.4 of the Tax Code of Ukraine.

An organization is considered non-profit only after it is entered into the Register of Non-Profit Institutions and Organizations. It remains there only as long as it strictly complies with the established rules. This is why the right to non-profit status is not a “default” characteristic, but a regime that requires systematic control.

Successful case: Accounting Support for Charitable Organizations: Assisting German Benefactors in Ukraine

Key Legal Requirements for Maintaining Non-Profit Status

Non-profit status operates on an “all or nothing” principle. An organization must comply with all provisions set out in the TCU at the same time. Violation of even one of them creates a risk of exclusion from the Register of Non-Profit Institutions and Organizations, even if the charitable foundation’s activities are in fact charitable, socially beneficial, and backed by an impeccable reputation.

The law establishes three basic conditions that must be met simultaneously.

Statutory Prohibition on the Distribution of Income

The founding documents must expressly prohibit the distribution of received assets, or any part of them, among founders, participants, members, employees, except for salary payments and the accrual of the Unified Social Contribution, members of governing bodies, and related parties.

At the same time, financing expenses related to the implementation of statutory activities, including administrative expenses, is not considered profit distribution, provided that such expenses are lawful and properly documented.

Liquidation Clause

The charter must also provide that, in the event of liquidation, merger, division, accession, or transformation, the assets are transferred to another non-profit organization of the relevant type or credited to the state budget.

Targeted Use of Funds

This is the broadest area for mistakes. All incoming funds must be used exclusively for the purposes defined in the charter. Going beyond the declared areas of activity, even with the best intentions or due to urgent necessity, is qualified as a violation.

Please note! During martial law, the application of non-profit rules has certain specific features defined by the transitional provisions of the TCU. They do not cancel the basic criteria, but they do affect the assessment of whether certain operations are permitted.

Why Charitable Foundations Are Excluded from the Register: Typical Violations and Practical Cases

In practice, charitable and other non-profit organizations most often lose their status not because of abuse, but because of incorrectly prepared documents, accounting errors, or a mistaken understanding of the limits of permitted activity. The key risks are concentrated in several areas.

Violation of Statutory Purposes

The most common situation is when a foundation starts carrying out activities that are not directly provided for in its charter. The argument is always the same: there was an urgent need, help was required, and amending the charter would take too long and be too complicated.

For example, a charitable foundation was established to support and provide treatment for children with rare diseases. The foundation’s charter provided for financing treatment, purchasing medicines and medical equipment, and organizing rehabilitation programs for children.

During an inspection, the controlling authority found that the foundation had used part of the charitable contributions to finance the construction and arrangement of a sports ground on the premises of an educational institution. This area of expenditure was not provided for by the foundation’s statutory purposes and was not related to providing assistance to children with rare diseases.

The controlling authority recognized these expenses as non-targeted use of funds, since the income of a non-profit organization must be used exclusively to implement the goals and areas of activity defined in its founding documents in accordance with Article 133.4 of the Tax Code of Ukraine. As a result, a corporate income tax liability may be assessed on the amount of such use, and the organization risks losing its non-profit status.

So the conclusion is clear: first amend the charter, then launch the new area of activity.

Distribution of Income Through Related Parties

The law allows foundations to hire employees, including founders, and pay them under contracts. However, such payments must be economically justified and properly documented.

For example, a foundation transferred funds every month to a sole proprietor who was the husband of the director for “consulting services.” There were no reports, acts of acceptance, or descriptions of the consultations. The tax authority qualified this as a hidden profit distribution in favor of a related party.

For the controlling authority, the absence of evidence that the services were actually provided is enough.

Another violation also worth mentioning is paying salaries to members of the foundation’s Supervisory Board or Management Board. In most charters, as well as under the law, their activities must be carried out strictly on a voluntary basis, meaning free of charge. If the tax authority sees remuneration paid to a Board member, this can lead to an immediate loss of status.

Administrative Expenses Exceeding the Limit

Charitable organizations are subject to a limitation: administrative expenses may not exceed 20% of annual income. However, many foundations do not keep separate records of such expenses or classify them incorrectly.

A real-life situation looks like this: a foundation received a large grant and decided to invest in development. It rented a representative office, hired a strong team, and launched an advertising campaign. At the end of the year, it turned out that administrative expenses amounted to 26% of income. The tax authority issued an order to eliminate the violations, putting the foundation on the verge of exclusion from the Register.

Ignoring financial limits is a very common ground for losing non-profit status.

Problems with the Charter

A charter that has not been updated for years may no longer comply with current legal requirements. In practice, foundations often continue working with documents that have remained unchanged for years, without responding to legislative changes. This is a risk that may stay hidden for a long time, but becomes critical during an inspection or liquidation.

For example, during the liquidation of one foundation, it turned out that the charter did not contain a provision on transferring assets to another non-profit organization. This made lawful closure impossible and led to lengthy court disputes with the tax authority over the fate of the foundation’s property.

Violation of Humanitarian Aid Accounting

A separate area of risk and increased attention is the accounting of humanitarian aid. The absence of proper accounting records for its receipt and use is effectively treated as non-targeted use.

A real case: a foundation received a large shipment of humanitarian aid from abroad but did not keep separate records of its distribution. When the tax authority requested a report, the foundation provided only general figures without the names of recipients or supporting documents. This became grounds for assessing corporate income tax on the full value of the goods.

All these examples have one thing in common: the problem does not arise at the moment of inspection, but much earlier, when decisions are made without a legal assessment of their consequences.

Successful case: Drafting the Charter of a Charitable Foundation for Importing Vehicles for the Ukrainian Armed Forces

The Cost of Losing Status: Financial Consequences and Reputational Reset

Exclusion from the Register of Non-Profit Institutions and Organizations means a complete change in the foundation’s tax regime and financial operating model.

After losing its status, the organization automatically moves to the general corporate income tax regime. This means that:

- all income of the organization may be subject to corporate income tax, including humanitarian aid, targeted funding, and charitable donations;

- tax liabilities may be assessed for all years during which the organization had non-profit status, if violations are identified;

- even if the organization did not actually generate profit, the controlling authority may assess additional tax liabilities based on statutory formulas and documented income.

In practice, the organization starts paying tax from resources that were raised to implement charitable programs.

In addition to the tax itself, penalties and late payment interest may also apply. In complex cases, the amounts of additional assessments can reach hundreds of thousands or millions of hryvnias, depending on the volume of incoming funds and the nature of the violations.

For many foundations, this means freezing programs, reducing the team, or urgently searching for funds to repay the tax debt.

The loss of status affects not only the tax model, but also the trust of partners and directly limits the organization’s opportunities:

- the foundation can no longer use the benefits of the non-profit regime, including corporate income tax benefits;

- it becomes more difficult to enter into agreements with government authorities or attract grants that require mandatory non-profit status;

- tax authority control increases, which requires additional spending on legal support and audits.

For a foundation, this is a point after which the entire architecture of its activity changes, from financial planning to the ability to attract resources. This is why we always emphasize that preventing violations is always cheaper than restoring status after it has been lost.

Legal Audit of a Charitable Foundation: Preventive Protection of Your Mission

Managers of charitable foundations think in terms of aid, results, and saved programs. But the tax authority evaluates not intentions, but documents, charter wording, accounting, and figures. It is precisely this gap between the mission and regulatory reality that creates risks.

Most problems can be identified long before an inspection. The only question is whether the foundation has systematic legal control rather than a post factum reaction.

Our team has been working at the intersection of corporate and tax law for more than 15 years. We think in terms of risk: not “is there a problem,” but “what consequences could it have in a year or during an inspection.” This is the strategy that allows us to protect the organization’s status, reputation, and resources.

For our clients, we conduct a comprehensive risk audit from the perspective of tax consequences and provide support that includes:

- analysis of the charter for compliance with the requirements of the Tax Code of Ukraine;

- review of internal policies, including remuneration, conflict of interest, and use of funds;

- assessment of risks in the foundation’s financial model;

- recommendations on bringing operations into full compliance with the law;

- support during tax inspections.

A legal audit by Pravova Dopomoha Law Firm is an investment in the foundation’s stability. It ensures that:

- documents comply with the law;

- the financial model does not create hidden tax risks;

- any inspection will confirm the legality of the foundation’s activities.

We do not simply correct mistakes. We create preventive protection that allows the foundation to effectively implement its aid programs without spending time and resources on the consequences of legal miscalculations.

If you manage a foundation and want to avoid tax problems and preserve non-profit status, contact us: fill out the online application on the website or call the phone number provided.

More about our legal support service for non-profit organizations is available here.