CFC: Submission of notification and report in Ukraine

Cost of services

Reviews of our Clients

... our work on joint projects assured us of your high level of professionalism

What we offer

-

Providing guidance on determining tax residency for individuals and the obligation to declare and pay taxes on Controlled Foreign Companies (CFCs), whether it arises in Ukraine or potentially in another country due to an individual's relocation amidst war.

-

Assessing the number of CFCs controlled by an individual and addressing the possibility of exempting them from taxation in Ukraine.

-

Offering expert consultancy on the taxation of controlled foreign companies in Ukraine: assisting in accurately identifying the controller, advising on potential tax exemptions, helping calculate the taxable base, and forecasting the tax liabilities in Ukraine (considering applicable legal adjustments). Informing about the controller's responsibilities, including the preparation and submission of CFC reports, among other aspects.

-

Assisting in preparing and submitting notifications for controlled foreign companies (to be filed within 60 days of establishing a CFC, changing ownership stakes, altering control mechanisms, or liquidating a CFC, etc.).

-

Providing support in completing and filing the CFC report by the deadline of May 1st each year following the reporting period.

-

Helping with the completion and submission of an abbreviated CFC report if a full report is not feasible or if the company's financial statement deadlines do not align with the filing requirements in Ukraine.

-

Assisting with the filing of amended or new CFC reports as necessary.

Furthermore, we offer comprehensive services for the support and annual maintenance of foreign companies, including assistance with opening bank accounts and the preparation and management of financial statements.

Documents Required

What are the benefits of filing a CFC notification?

If you've made the decision to return to Ukraine or maintain your tax residency there, filing a CFC (Controlled Foreign Company) notification offers a valuable opportunity to avoid penalties for non-compliance (the tax authorities will become aware of your foreign company after the first exchange of tax information in 2024).

So, it's a perfect time to conduct a thorough review of all your companies, solidify your future plans regarding tax residency, and proactively prepare for reporting.

What are the penalties for violating CFC regulations?

Failure to adhere to CFC rules can result in penalties of up to UAH 2.5 million, depending on the nature of the violation.

What are the deadlines for submitting CFC notifications?

You have a 60-day window to submit the notification from the following events:

- Establishing a CFC

- Acquiring actual control over a CFC

- Changing your ownership stake in a CFC

- Liquidating a CFC

- Ceasing actual control over a CFC, and so on.

When should you file the CFC reports?

The CFC reports must be filed by May 1st of the subsequent year, following the reporting year.

Service packages offers

- introductory consultation

- determination of tax residency of an individual

- analysis of documents of a foreign company and preparation for filling out the notification

- filling out a notice of CFC based on the registration data of the client's company, including in the taxpayer's electronic cabinet

- consultation

- determination of the tax residency of an individual

- analysis of corporate documents and financial statements of an individual

- analysis of operations of a foreign company in the reporting period (analysis of primary documentation), in order to determine whether it is necessary to make adjustments to the financial result of the CFC

- calculation of the CFC tax base, forecast for tax payable

- filling out the declaration and submitting the declaration

- submission of an abbreviated report on the CFC (if the financial periods of the CFC do not coincide with the deadlines for filing a declaration in Ukraine for an individual, or if there are no financial statements of the CFC as of the date of filing the declaration)

- submission of an updated CFC report (if incorrect reporting was submitted on time)

- submission of a new reporting report on the CFC (if a report with errors was submitted, but the deadline for filing a report on the CFC has not yet passed)

- tax payment control

- consultation

- determination of the tax residence of an individual (especially for individuals who left Ukraine in connection with the war) in order to find out whether they are really subject to Ukrainian rules on CFCs

- audit of all foreign companies, analysis of their functional load in order to identify unnecessary companies

- support in the liquidation of unnecessary CFCs

- business model restructuring

- restructuring of CFC ownership

- change of tax residence of an individual

Procedure for submitting a notification for CFCs

In order to submit a notification for controlled foreign companies, we will require the following essential information about the company from the client:

- Registration details

- Company structure

- Ownership format (direct or indirect ownership)

- Information about the triggering event that necessitates the notification (establishment of CFC, changes in ownership percentage, liquidation, etc.)

The notification for CFCs is submitted electronically through the taxpayer's online portal.

Individual residents of Ukraine or legal entities resident in Ukraine are obligated to inform the regulatory authority (i.e., submit the mentioned notification) in the following circumstances:

- Each instance of directly or indirectly acquiring a stake in a foreign legal entity or commencing effective control over a foreign legal entity, resulting in the recognition of such individual (or legal entity) as a controlling entity according to the requirements of the current article.

- Establishment, creation, or acquisition of property rights to a share in the assets, income, or profits of an entity without legal entity status.

- Each occurrence of disposing of a stake in a foreign legal entity or ceasing effective control over a foreign legal entity, leading to the loss of recognition of such individual (or legal entity) as a controlling entity in accordance with the requirements of the current article.

- Liquidation or disposal of property rights to a share in the assets, income, or profits of an entity without legal entity status.

Submitting a Notification for CFCs

No documents are required to be submitted to the tax authorities. Only the CFC notification form needs to be filled out and submitted electronically. Our team of lawyers will handle the preparation and submission of the CFC notification on behalf of our client.

Procedure for filing the CFC Report

The CFC report is submitted electronically through the taxpayer's online portal.

Documents required for filing the CFC Report

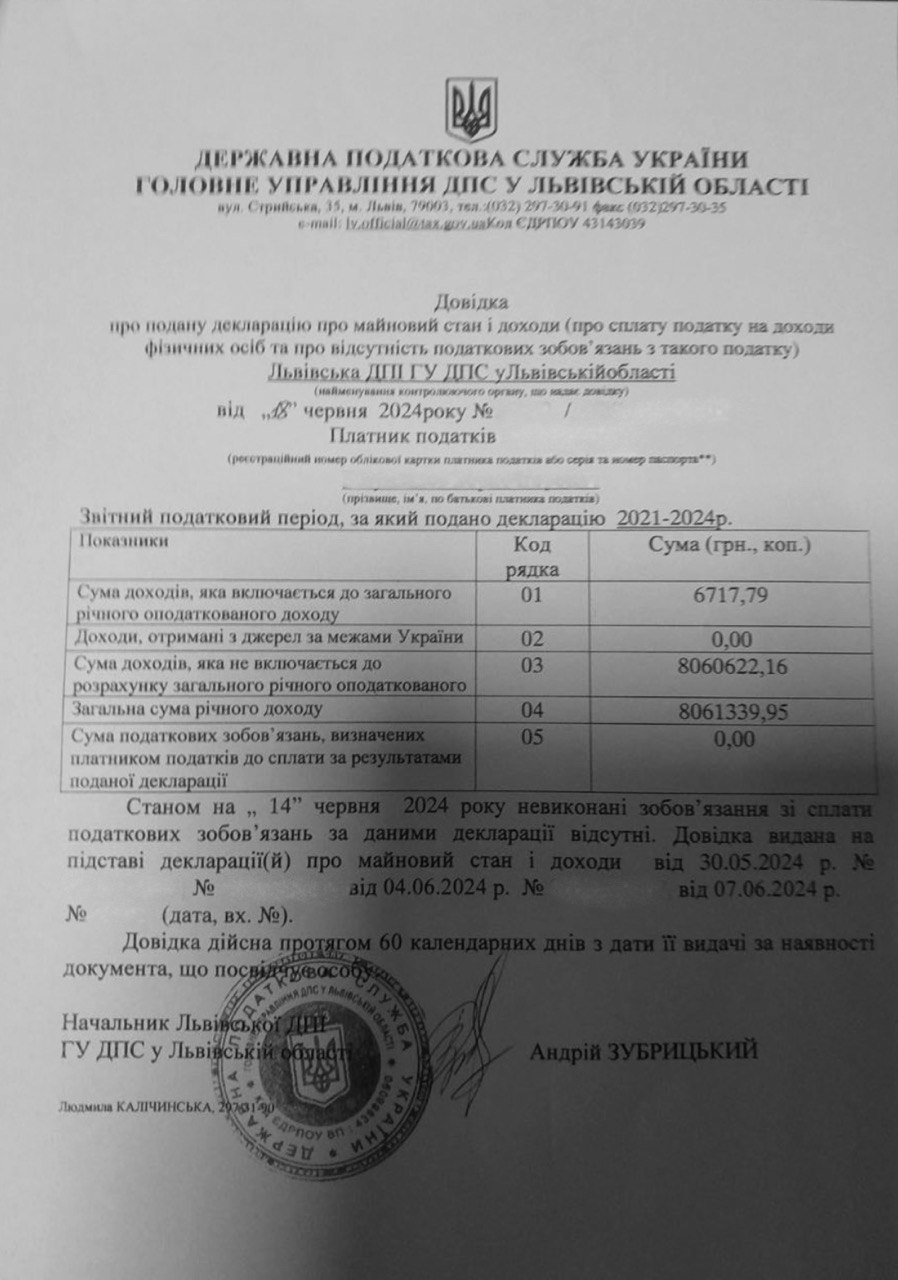

The key document to be submitted is the financial statement for the CFC, covering the reporting period. This statement verifies the income amount and the tax paid by the company in its country of registration. The financial statement of the controlled foreign company will undergo an audit.

The report should include the following information:

- Name, address, legal structure, tax registration numbers (if applicable), and state registration numbers of the Controlled Foreign Company.

- Percentage of ownership held by the controlling entity in the Controlled Foreign Company.

- Ownership structure of the shares in the Controlled Foreign Company in case of indirect ownership.

- Revenue details from the sale of goods, provision of services, and pre-tax profits based on the financial statement.

- Calculation of the adjusted profits of the Controlled Foreign Company as per the requirements, including the portion included in the overall taxable income of the controlling entity.

- Information on the grounds for exemption from taxation of the Controlled Foreign Company profits, as per the relevant provisions.

- Dividends received by the Controlled Foreign Company directly or indirectly through subsidiary entities from Ukrainian legal entities.

- Profits actually paid to the controlling entity by the Controlled Foreign Company.

- List of transactions between the Controlled Foreign Company and related non-resident parties.

- Number of employees in the Controlled Foreign Company at the end of the reporting (tax) year.

- Information on the profits derived by the Controlled Foreign Company from a permanent establishment in Ukraine.

Rest assured, we will handle the report preparation for your controlled foreign companies and ensure its timely submission. In case any challenges arise, we will minimize risks and provide comprehensive support to our clients.

Why us

Our clients

Our successful projects

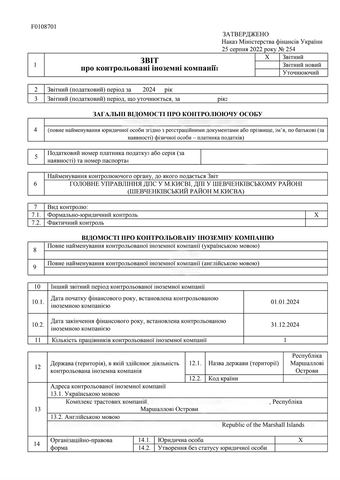

Notification Form for Controlled Foreign Companies

The notification is submitted electronically in the form of a report that includes essential details about the CFC (registration information, ownership stakes, and so on).

How can you determine if CFC regulations apply to you?

If you have a direct or indirect ownership stake in a foreign company/companies or if you exercise actual control (e.g., managing a bank account, providing instructions to the company's director regarding mandatory actions, or holding a general power of attorney), then you are considered a controller of CFCs.

A CFC refers to a foreign company that is controlled by you, either legally or in practice.

Preparation of CFC financial statements and conducting audits.

The financial statements (audited) must be submitted alongside the CFC report. We can assist you with preparing the financial statements, conducting audits, and providing support in calculating any additional taxes payable in Ukraine.

Declaration of CFC profits.

This is a mandatory requirement, even if the company is exempt from taxation in Ukraine. It is necessary to declare the ownership of the company regardless of its tax-exempt status.

Answers to frequently asked questions

Where should a notification about acquiring or ending involvement in controlled foreign companies be sent?

It should be sent to the tax authority at the location where the individual controlling the foreign company is registered for tax purposes.

How can a report on controlled foreign companies be submitted?

The report can be electronically submitted through the taxpayer's online account.

Under what circumstances are taxes not required to be paid for a controlled foreign company (CFC)?

The law provides several situations in which a CFC may be exempt from taxation:

- If it is a publicly traded company.

- If it is a registered charitable organization.

- If the combined income of all CFCs controlled by an individual does not exceed 2 million euros per year.

- If there is a double taxation avoidance agreement between Ukraine and the country of registration, and the corporate income tax in the country of registration is at least 13%, or if the active income constitutes at least 50% of the total income.

How is the 2 million threshold calculated for tax exemption of CFCs?

For example, if an individual owns a 35% stake in a Cypriot company and a 100% stake in an Estonian company, and the Cypriot company's gross income for 2022 was 1.5 million euros, while the Estonian company's income was 200,000 euros, the calculation is as follows:

- 1.5 million euros x 35% = 525,000 euros (this is the income attributed to the individual's share in the Cypriot company)

- 525,000 euros + 200,000 euros = 725,000 euros, which is clearly below the 2 million euro threshold. As a result, the individual's CFCs are eligible for tax exemption, although they still need to be declared.

Do you have to pay taxes on the profits of an Estonian company owned by a Ukrainian beneficiary?

In this case, we need to consider the exemption criterion mentioned earlier, which is #4. Here's the breakdown:

- here is a double taxation avoidance agreement between Ukraine and Estonia.

- The corporate income tax rate in Estonia is 20%, which is clearly higher than the 13% threshold set by the legislation. However, since the Estonian company de facto does not pay corporate income tax (in most cases, until profits are distributed to the shareholder), the Ukrainian tax authority is likely to consider the effective tax rate of the Estonian company as 0% instead of 20%.

- If the Estonian company is actively engaged in trading (selling goods, providing services), and more than 50% of its income comes from active trading activities, it can be considered to meet the sub-criterion 2) and may be exempt from taxation.

Can "passive" companies with a corporate tax rate below 13% in the country of registration be exempt from taxation?

Yes, but only if they can substantiate their substance, meaning they can demonstrate real economic presence in the country of registration, such as having an office and employees. In other words, if they can prove that generating passive income is their professional activity.

Will transferring the ownership of a controlled foreign company to relatives help avoid the requirement to declare it?

No, it will not.

Can avoiding the requirement to declare a Controlled Foreign Company (CFC) be achieved by distributing ownership among multiple individuals with each holding a share of less than 10%?

No, that strategy will not work if all the individuals are Ukrainian.

Do you have to pay taxes on the profits of a CFC if it has not distributed any dividends?

Yes.

Do dividends paid out reduce the taxable base of the CFC in Ukraine?

Yes.

If foreign company-1 is owned by foreign company-2, do you only need to declare foreign company-1 as a CFC?

No, both foreign companies need to be declared as CFCs.

How can you legally avoid having a CFC?

- Liquidate the CFC if it lacks significant functional significance (a thorough review of all companies and understanding their actual purpose is required).

- Change tax residency (which is relatively straightforward nowadays, considering that many of our fellow citizens have already moved abroad).

- Establish a business with foreign partners.

How will the Ukrainian tax authority become aware of my CFC?

Starting in 2024, there will be an exchange of financial information with tax authorities of other countries. This exchange will include financial data, including accounts held by foreign companies, which will be collected and transmitted to Ukraine.

If you need to make a decision regarding your CFC, feel free to reach out to us!

We can help determine if you are required to pay taxes on your CFC and to what extent. Additionally, we can assist you with submitting notifications and reports related to your CFC in Ukraine.