Essence of leasing and the most popular types of it

Cost of services:

Reviews of our Clients

... our work on joint projects assured us of your high level of professionalism

Providing of leasing services is actual topic during an economic crisis. A leasing is one of the most effective ways to give equipment, machines (main assets) for entrepreneurs, who don’t have enough money, in a temporary paid usage. Except it, a lessee gets a right to buy back this property after a term of a lease agreement is finished. In this article we will try to examine what leasing is and what the difference between the most popular types of it– operational and financial one.

A concept of leasing you can find in a few legal acts. According to the Civil Code of Ukraine a lease agreement is transferring of own property in a temporary paid usage from a lessor to a lessee which was bought by the prior consent of a lessee or without it. The Commercial Code defines it like an investment activity when a lease object is transferred in a temporary paid usage. The Tax Code has a definition of it as an operation. Considering abovementioned terms we can say that a leasing is a transferring of a property, which can be bought or produced specially for a lessee by the prior consent with a lessor or without it, in a temporary paid usage.

At the same time the Tax Code defines one more feature of a leasing – it is a property which can be an object of leasing. It can be only main assets which are used by entrepreneurs for their business activity. For example, it can be equipment for production, vehicles, devices and inventory. The main features of these material assets are that their cost will be decreased according to a physical or moral wear and tear and term of their usage is more than one year. If main asset’s cost is less than 6 000 UAH than it is not considered as a main asset.

We start to analyze main types of a leasing according to the current laws after we look through the general features of a leasing. The most popular types are operational and financial leasing. If financial leasing is regulated by a specific Law of Ukraine “On a financial leasing” then operational leasing is regulated by separated clauses of different legal acts. Abovementioned Law doesn’t give a clear understanding of a financial leasing’s specify. Only with a help of clauses of the Tax Code we can find the main differences between an operational and financial leasing. An operational leasing it is a commercial operation of an individual or legal entity which transfers to a lessee some main assets, bought or produced by a lessor on different from a financial leasing terms. As follows there are no special features of this type of a leasing. In return we can examine features of a leasing when it is considered as a financial one.

The first feature of a financial leasing is that its object is transferred for a term when not less than 75% of its prior cost will be depreciated. It means that if prior cost is depreciated less than 75% then it is an operational leasing. While characterizing this feature, we can talk about another one. If a residual value is not more than 25% of a prior cost when agreement’s term is finished then it is a financial leasing.

Another leasing feature also related to a prior cost of a leasing object. If total amount of lessee’s payments is equal or is overtopped that a prior cost then there is a financial leasing.

As it was said previously, an operational leasing can be provided by individuals and legal entities, while a financial leasing can be provided only by legal entities.

The next feature is that lessee must buy back an object for a defined price according to a lease agreement during its validity term, while an operational leasing doesn’t demand this term.

The last one feature of a financial leasing is unique of an object which was bought or produced specially for a lessee. Property is produced\bought, considering technological features which are necessary for a lessee. It means that this object can’t be used by another person, except a lessee. An operational leasing object can be used not only by a lessee but also by other people.

The legislative doesn’t take an opportunity from parties to define a leasing as an operational one even it doesn’t have abovementioned features. In this case you must wright it down in an agreement. Pointing this type of operation, it can’t be changed in the future. Drafting agreement’s terms, be attentive and don’t take an operational leasing for a usual rent. According to the Civil Code of Ukraine they have a lot of differences which are related to targets, object, way of gaining ownership right by a lessor or by a landlord etc.

A practical side of distinction of operational and financial leasing agreements is tax nuances which are defined by the Tax Code of Ukraine and by the Order of the Ministry of Finances of Ukraine “On approving Principles (standards) of accounting 14 “Rent”. In spite the fact that a right of financial leasing object’s disposal is belonged to a lessor, it will be on a lessee’s balance. As follows, calculated amortization will decrease lessee’s profit for taxation because of using main assets. Except it, lessee also gets a credit for a VAT of an object price instead of a lessor. Also you should keep in mind that a lessee has a guaranteed right to buy back a financial leasing object after finishing term of an agreement. So that’s the practical aspects of distinction of operational and financial leasing agreements.

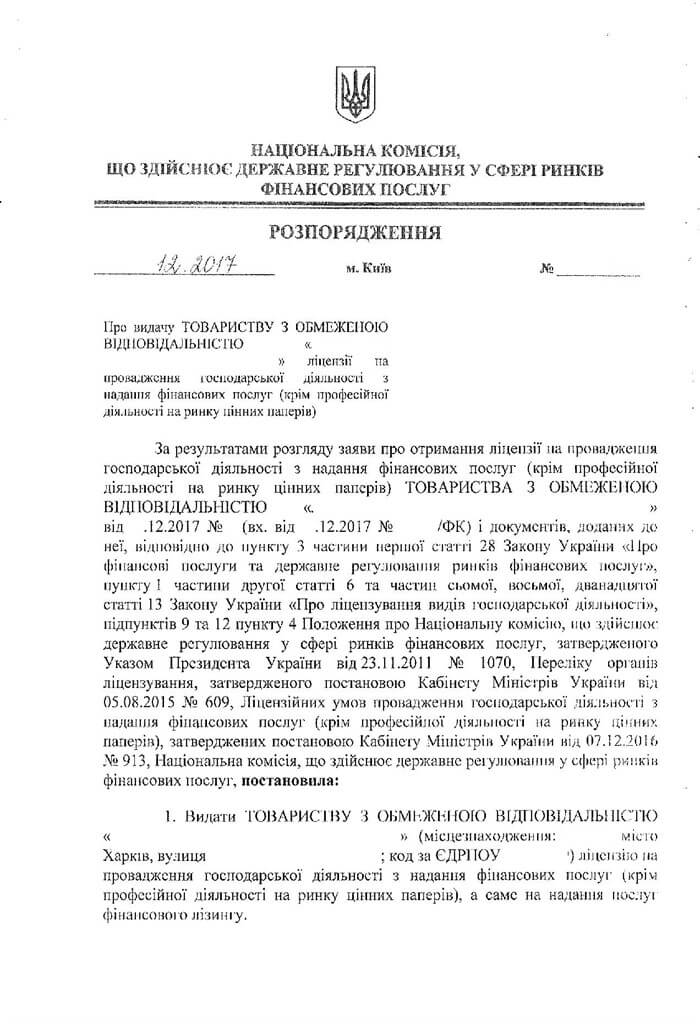

The legislation doesn’t demand necessity of getting a license for an operational leasing directly. Analyzing legal acts in this sphere, we can make a conclusion that, unlike a financial leasing, an operational leasing doesn’t have to be licensed. The licensing body also points that only a financial leasing must be licensed before providing services.

So we examined features of a leasing and the most popular types of it. You can read about our services on getting a license for a financial leasing via the link.